|

Industry News: China's Personal Care Market Ushers in a New Pattern, and Douyin E-commerce Has Become a New Engine for Industry Growth Recently, Nielsen IQ released the "Trends and Prospects Report of China's Beauty and Personal Care Industry," delving into the consumption trends and emerging growth points in China's beauty and personal care market in 2023. With consumers' continuous pursuit of quality living and the maturing concept of skincare, the Chinese beauty and personal care market is witnessing a new development pattern.

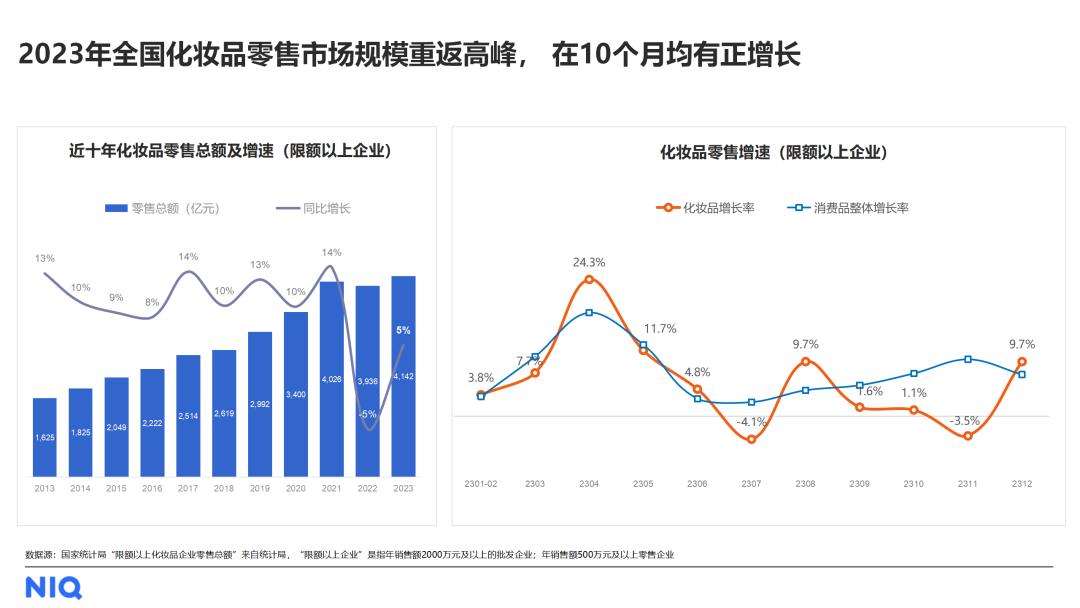

According to data from the National Bureau of Statistics, the retail scale of cosmetics in China steadily rebounded in 2023, reaching a peak of 414.2 billion yuan for the whole year. Ten months of the year showed positive growth, indicating the recovery and transformation of consumer demand.

Continuous Growth in Skincare Market, Online Channels and Department Store Counters Leading the Way

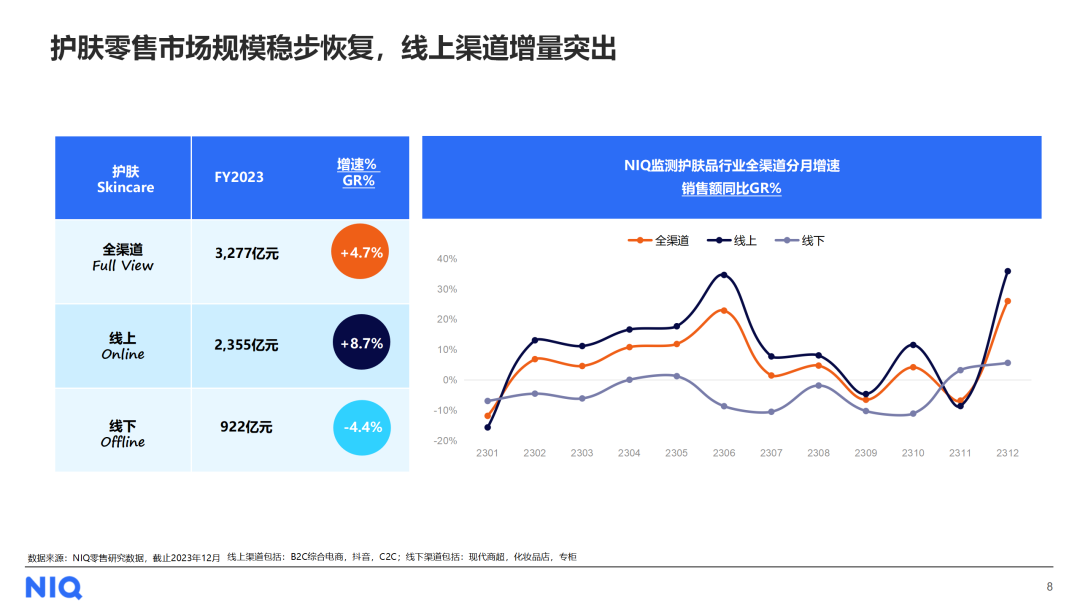

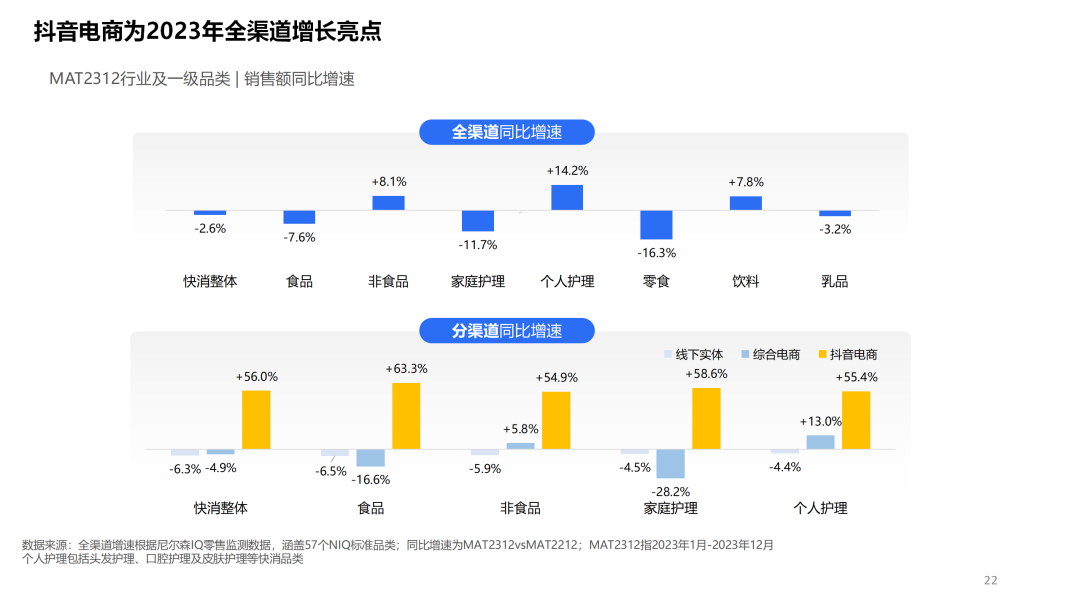

The report points out that consumers' pursuit of quality living and skincare concepts continues to mature. According to Nielsen IQ's monitoring of the skincare industry's omni-channel data, the annual sales scale of the skincare market in 2023 reached a cumulative total of 327.7 billion yuan, a year-on-year increase of 4.7%. The growth rate of online channels was 8.7%, while offline channels saw a growth rate of -4.4%. Among them, online channels, especially Douyin e-commerce platforms, showed significant growth, with an annual growth rate of 56.6%, becoming a new engine for online growth in the beauty and personal care industry. While the growth rate of offline channels was relatively modest, department store counters showed impressive growth, demonstrating consumers' continued pursuit of high-quality skincare products, while modern channels (such as supermarkets) and cosmetics stores showed a shrinking trend.

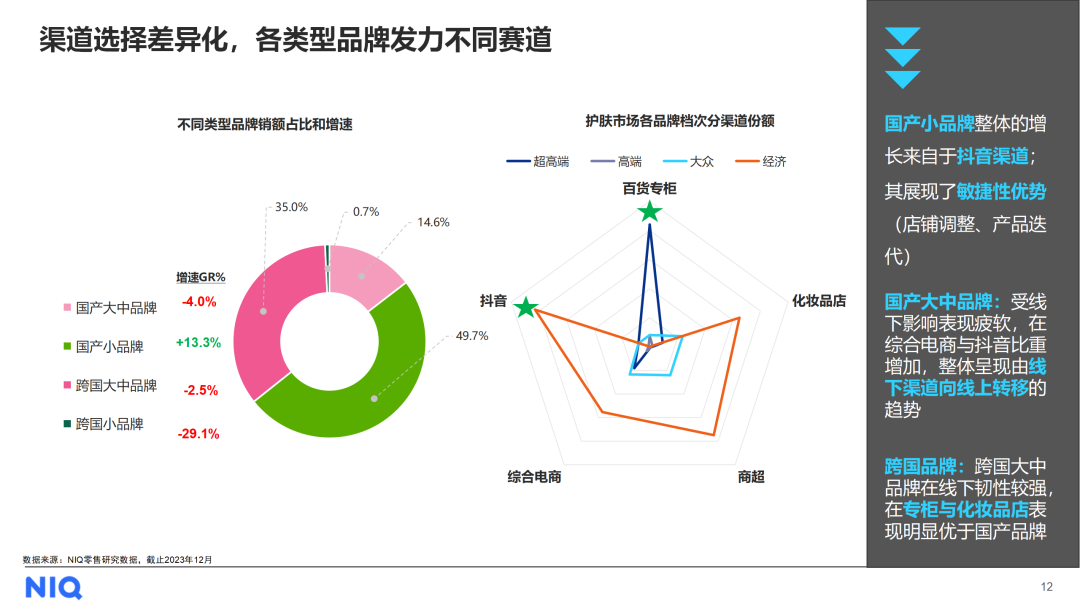

With differentiated channel layouts, the channel strategies of different grades of brands are also showing a trend of differentiation. Ultra-high-end and economy brands have become the main drivers of market growth, while the market share of mid-range brands has been somewhat squeezed. In the post-pandemic era, consumers' purchasing power has become polarized, with some continuing to pursue high-end products while others choose to downgrade their consumption. This change poses new challenges for brand positioning and product strategies.

In terms of brand ownership, domestic brands account for over 60% of the skincare market, with sales increasing by 8.8% compared to last year. Sales of multinational brands have contracted slightly. The market share of small brands with sales below 100 million yuan reached 50.5%, a year-on-year increase of 12.3%. Domestic small brands play an important role in the growth of the domestic skincare market, rapidly rising with the support of Douyin channels.

The report also provides a detailed breakdown of category rankings in different channels. Major skincare products such as essences, lotions, creams, and eye creams are the main categories in each channel, with the category layout of modern supermarkets and Douyin being closer, while cosmetics stores and department store counters show a similar trend. In offline channels, cosmetics stores and modern supermarkets are indispensable places, especially for third- and fourth-tier cities. The report also points out that the pandemic has accelerated the transformation of this channel, with brands and retailers seizing trends and focusing on product strength to empower brands with a sense of technology and emotional value, enabling stores to adopt a service model of sales + professional care.

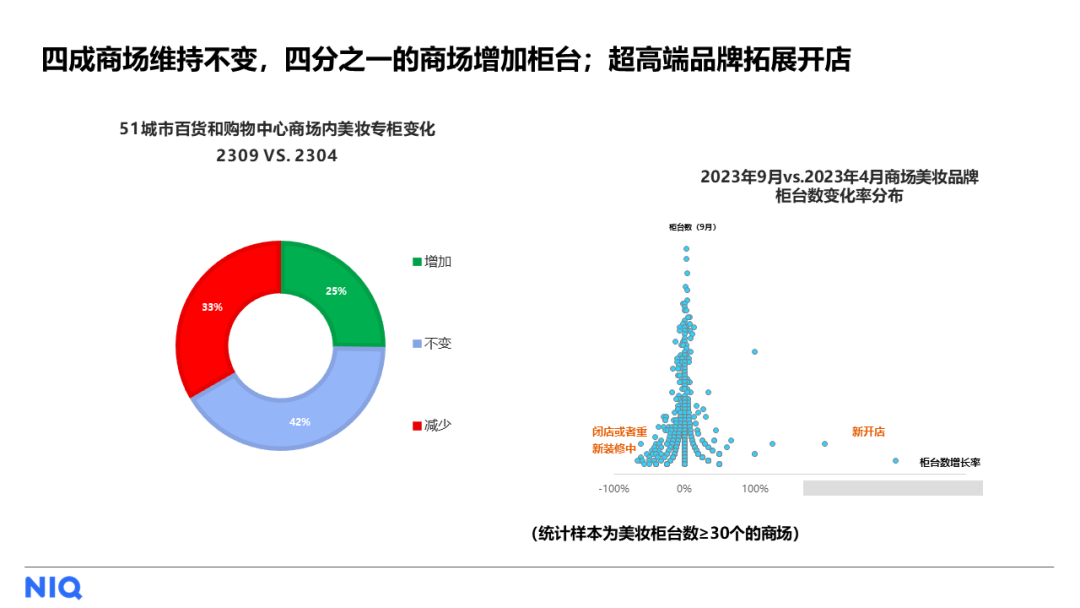

Shopping malls are experiencing a polarization trend in new store openings, with more counters added in high-end and low-end positioned malls. The phenomenon of traditional department stores removing counters is widespread, with mass-market malls being the most affected. Overall, four out of ten malls have the same number of counters, and one-fourth of malls have added counters, mainly from ultra-high-end brands.

Douyin E-commerce Rising, Leading a New Track in the Skincare Industry

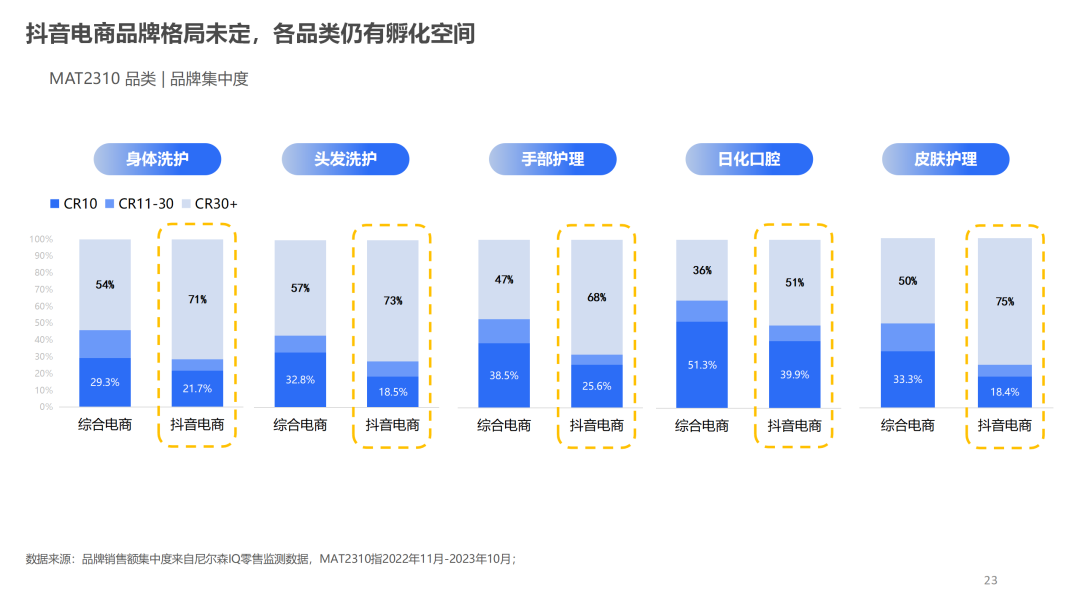

Against the backdrop of a slightly sluggish overall omni-channel growth rate of fast-moving consumer goods in China in 2023, the personal care sector has shown strong growth momentum. Among them, Douyin e-commerce, as an emerging channel, has brought unprecedented development opportunities to the skincare industry. It is reported that categories such as hair care, oral care, and skincare in the personal care sector have achieved high-speed growth on Douyin e-commerce, with growth rates exceeding 50%, demonstrating the huge potential of Douyin e-commerce in the skincare industry. From the perspective of brand concentration, Douyin e-commerce has become the main battleground for small and medium-sized brands. In categories such as body care, hair care, and skincare, Chinese local small and medium-sized brands ranked 30 or above have a concentration on Douyin e-commerce of over 70%, a figure much higher than other channels such as comprehensive e-commerce. This indicates that Douyin e-commerce provides a broader stage for small and medium-sized brands, enabling them to compete on the same platform as large brands and share the market dividends together.

In terms of price, skincare products priced below 200 yuan contribute the highest proportion of sales on Douyin e-commerce, reaching 83%, and maintaining a high growth rate of 56%. This data not only reflects consumers' pursuit of cost-effectiveness but also highlights the advantages of Douyin e-commerce in promoting economical skincare products. Meanwhile, brands of all levels maintain positive growth on Douyin e-commerce, with both ultra-high-end and economical brands growing by over 50%, demonstrating the inclusiveness and attractiveness of Douyin e-commerce to brands of different levels.

About Us The total value of the personal care market is forecasted to reach 607 billion RMB by 2028. As the personal care market becomes increasingly diverse, new opportunities are likely to emerge in more segmented categories, challenging the dominance of established companies and allowing niche brands to develop rapidly. So, how can one find paths to business growth in the new year?

The 2024 6th Shanghai International Personal Care Expo (referred to as "PCE Personal Care Expo") is committed to "creating a new ecosystem for personal care," continuously integrating global resources to help personal care companies achieve new growth. It will be held from August 7-9, 2024, at the Shanghai New International Expo Centre. Linked with the PCE Personal Care Expo Guangzhou, which will be held from March 4-6, 2025, at the Nan Fung International Convention & Exhibition Center in Guangzhou, the expo brings together manufacturers from the entire industry chain to showcase cutting-edge technology and new products in the personal care field, providing a one-stop sourcing service. Additionally, to assist personal care companies in expanding their international markets, overseas exhibitions will be held from June 4-6, 2024, at the Jakarta International Expo in Indonesia, and from December 17-19, 2024, at the Dubai World Trade Centre in the UAE. These events aim to help personal care companies explore global markets and achieve dual circulation in domestic and international markets.

|

|

LinkedIn:Personal Care Expo (PCE) LinkedIn:Personal Care Expo (PCE) Ins:yinghezhanlan Ins:yinghezhanlan Facebook:Pce Yinghe Exhibition Facebook:Pce Yinghe ExhibitionPrivacy policy 沪ICP备17037700号 |